Let’s be honest—when you’re juggling daily priorities and a never-ending to-do list, audit risk probably isn’t the first thing on your mind. And hey, maybe the “out of sight, out of mind” approach feels easier. After all, it doesn’t exactly scream excitement, and there’s always something more urgent to handle.

But here’s the thing: while this post won’t try to convince you to put audit risk at the very top of your list, it will show you why it deserves a spot on your radar. Understanding audit risk—even just the basics—can go a long way in helping you plan effectively and avoid surprises. And with a few simple steps, you can set yourself (and your audit) up for success.

What Is Audit Risk?

Companies are facing increased risk every day, often arising from economic, financial, technological and security threats, and other uncertainties. A common measure companies use to mitigate against such risks is to engage an audit firm to conduct an independent audit, such as a SOX/financial statement audit, security audit, SOC 1 or SOC 2 audit, etc. While audits are a great countermeasure to risk, how do you determine audit risk? Specifically, is there a risk that your SOC 1 or SOC 2 auditor did not express a fair or accurate opinion? Is there a risk of material misstatement?

According to the American Institute of Certified Public Accountants (AICPA), audit risk is defined as follows: The existence of audit risk is recognized in the description of the responsibilities and functions of the independent auditor that states, “Because of the nature of audit evidence and the characteristics of fraud, the auditor is able to obtain reasonable, but not absolute, assurance that material misstatements are detected.”

Previously, we have discussed the concept of reasonable assurance in auditing, which means that even the best auditors are unable to 100% certify that internal controls at the service organization were designed and operated effectively to achieve the stated control objectives (SOC 1) or service commitments and system requirements based on the applicable Trust Services Criteria (SOC 2). Enter audit risk.

How Is Audit Risk Defined?

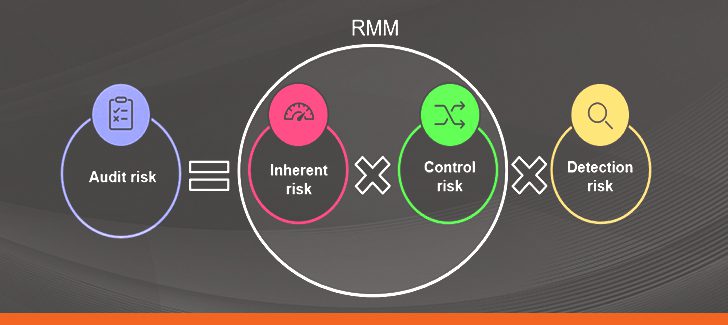

Audit risk can be defined by the audit risk model (see image below). Simply put, audit risk is a function of inherent risk, control risk, and detection risk. Inherent risk is the risk of misstatement if no controls are applied, whereas control risk is the risk that an organization’s controls will not prevent or detect a misstatement. Detection risk is the risk that the auditor will not identify a material misstatement.

What Is the Audit Risk Model?

The formula for the audit risk model is as follows:

Image Source: aicpa-cima.com

Inherent risk, control risk, and detection risk are the components that make up audit risk. Risk is inherent in every business, process, and transaction; it’s the reason internal controls must be established. However, there is a risk that the right controls were not identified or sufficiently applied to mitigate against the inherent risk in your business, processes, and transactions, which is your control risk. Further, there is a risk that even once the proper controls are applied, the auditor did not perform sufficient control testing to determine the adequacy of the design and operating effectiveness of controls (detection risk). This combination of factors is the basis of audit risk.

Understanding the Audit Risk Model: How It Works in Practice

The audit risk model isn’t just theoretical; it’s a highly practical framework that guides how organizations assess, manage, and audit risk. In real-world settings, including IT compliance and SOC auditing, the model provides a structured way to understand where risk exists and how to mitigate it effectively.

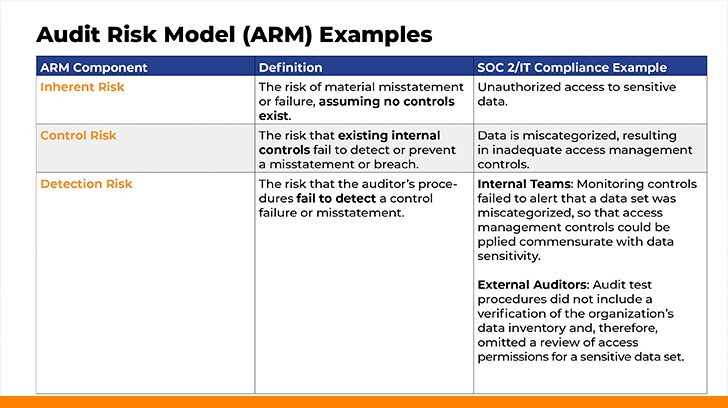

In my previous role leading risk and compliance for a financial technology company, I used the audit risk model to shape our internal control strategy. It helped us prioritize resources, align our controls with the areas of highest inherent and control risk, and ensure we were truly audit-ready, not just checking boxes. How do you use the audit risk model? The table below illustrates the audit risk model (ARM) formula with definitions and examples relative to SOC 2/IT compliance.

As illustrated above, the ARM can be useful both to organizations and their external auditors. Organizations can apply the ARM proactively to design a risk-based internal control program and prepare for external audits like SOC 1/SOC 2, ISO, or financial statement audits. The ARM helps them identify where controls are needed, how strong those controls must be, and where audit resources should be focused as they prepare for the audit. The ARM can also be helpful as organizations evolve and grow. For example, many of my clients have evolved from their initial start-up days when we first conducted their SOC 2 audit. As their organizations have grown and become more complex, and as new technologies and vendors have been incorporated into their systems/services, we have found that it makes sense to periodically revisit the ARM to identify new risks and controls, and evolve existing controls to ensure the right controls are in place to mitigate the risk to the organization.

At the other end of the spectrum, auditors use the ARM to plan and perform the audit. The ARM is a critical mechanism for reducing audit risk. They evaluate inherent risk and control relative to the client’s environment, and adjust detection risk by modifying the nature, timing, and extent of audit procedures (e.g., by performing more testing in higher-risk areas).

What Are the Types of Audit Risks?

In the case of a SOC 1 report or a SOC 2 report, audit risk is typically the result of one of two types of misstatements, defined as follows:

- Known misstatements: these are fact-based misstatements, due to factors such as incorrect data selection, errors in the information obtained/processed, or a misinterpretation of the data.

- Likely misstatements: these are judgment-based misstatements that are the result of a discrepancy between management’s and the auditor’s perception of the data or evidence obtained as part of the audit.

The AICPA has identified common scenarios from which audit risk arises. Many of the identified scenarios relate to financial statement audits, but in the case of SOC 1 and SOC 2 audits, the following are common contributing factors to a misstatement:

- An inaccuracy or error in gathering or processing data,

- The omission of relevant evidence or data elements,

- The omission of information required to be disclosed as it relates to the relevant SOC 1 control objectives or SOC 2 criteria,

- Management or auditor oversight or misinterpretation of facts, and

- Management or auditor judgments related to the evidence or data gathered in support of the audit.

How Do You Identify & Reduce Audit Risk?

Can audit risk be zero? While it’s not realistic to think you can eliminate all risk, with proper audit planning, you can effectively reduce and mitigate against audit risk. Here are some recommendations to keep on hand in order to set your next audit up for success.

Engage a Reputable Auditor

It’s easy to fall into the trap of choosing an auditor based on fees alone, or to rely too heavily on a “SOC Checklist” one-size-fits-all approach to your audit. You should evaluate the credentials of any audit firm you are considering engaging with, such as whether they are a registered CPA firm, the experience of the firm’s partners and staff, including their experience with similar clients in similar industries, and the firm’s review processes, including independent review protocols.

Conduct a Risk Assessment

A proper risk assessment should already be a key element of your company’s strategy and internal control framework, but it’s also critical in supporting an effective audit. A proper risk assessment will help to ensure that your SOC audit is properly scoped – that the suitable criteria (i.e., control objectives, controls, policies, procedures, laws, and regulations, etc.) selected in the audit are appropriate and will meet the broad needs of the users of your report (a.k.a., your clients). Likewise, assuming you completed task #1 above, your auditor should also conduct their own risk assessment to facilitate proper audit planning. SOC 1 and SOC 2 audits should always be tailored to the client’s industry and business, and a risk assessment is key in identifying which systems, processes, and controls should be included in the audit. Again, avoid the checklist/one-size-fits-all approach.

Ensure Adequate Audit Planning

Building off #2, sufficient time should be allocated to properly plan the audit. Have the proper control objectives/criteria been included in the audit plan? Have all the relevant systems been identified? Are the right processes and controls in place to achieve the stated control objectives and criteria? What evidence will be presented to determine the design and operating effectiveness of controls? What external and industry factors are present that may impact the audit approach? The risk of misstatement can often be attributed to errors or omissions relative to the identified systems, controls, and audit evidence, so it’s worth the time spent upfront to adequately scope and plan the audit.

Foster Audit Transparency

Being audited is never fun, and it’s natural to want to do whatever it takes to get through the audit as quickly as possible with no findings, issues, or problems. However, it’s important to be transparent throughout the audit process by not only describing the controls and processes that are in fact adequately designed and effective, but also alerting your auditor where errors may be present. A worse scenario than disclosing known findings to your auditor during the audit (a requirement in management’s representations and assertions) is an undisclosed error that turns into a misstatement, breach, adverse or qualified opinion, or other issue that causes harm to your business and your clients.

What Is Acceptable Audit Risk?

The key to determining an acceptable level of risk is to apply the concepts of the audit risk model. Striking an appropriate balance of inherent risk, control risk, and detection risk will result in a suitable audit plan that reduces the risk of material misstatement. Proper planning, an adequate risk assessment, and an appropriate mix of preventative and detective controls will help to design an audit plan that allows the auditor to form a reasonable basis for their audit opinion. It’s important to remember that there is a certain degree of judgment involved on both the part of management and the auditor. The end result is not black and white, which is why choosing a quality auditor is so important!

Your Next Steps in Managing Audit Risk

Are you concerned your audit has not been properly planned or scoped? Do you fear your audit risk is at an unacceptable level? Does it concern you that even with proper planning, a fair amount of judgment is involved? Contact the team of audit professionals at Linford & Company, and we can answer your SOC 1 audit, SOC 2 audit, and risk-related questions to get you on the right track.

Maggie has over 15 years of experience in Risk Management and IT Compliance. She spent nearly 10 years in KPMG’s IT Advisory and Attestation practice before joining a financial technology company as the Risk and Compliance Director. She has overseen numerous SOC 1 / SOC 2 audits and other IT Compliance audits and has vast experience implementing risk management and IT compliance solutions. She is Certified in Risk and Information Systems Control (CRISC) and obtained a Bachelor of Science in Business Administration, Finance, from the University of Colorado at Boulder.